by John McCarthy Consulting Ltd. | Aug 3, 2021 | Blog, News

The Coronavirus (COVID-19) has caused auditors to develop new techniques in carrying out their audit work, mainly involving greater use of technology. In this, the first blog of our three-part series, we will look at some recent audit monitoring inspection reports that have highlighted the most common problem areas for auditors.

Stock Attendance (ISA 501)

Many firms have not been able to attend clients’ premises for inventory counts. In these circumstances the auditor must attempt to perform alternative procedures e.g., where the client takes a live video call from the auditor and ‘walks’ the auditor remotely through the stock count location. Details of alternative procedures like this, and the auditors’ conclusions following the procedures, must be documented on the audit file. If adequate alternative procedures cannot be performed the audit file needs to document a consideration of the impact on the auditor’s report.

Where audit clients have not traded for significant periods of time, the audit file needs to show some consideration of potential stock impairment or obsolescence. A sceptical approach by auditors is always prudent. The ICAS has issues excellent guidance on attendance at stocktakes during the coronavirus outbreak. It’s worth looking at.

Fraud (ISA 240)

Audit files should fully document consideration of fraud (including the scope for fraud involving Government Covid subsidies/grants), especially where the audit firm may not have direct access to its audit client and/or where audit clients may not have direct access to their customers.

Common findings on monitoring visits include poor or inadequate completion of fraud checklists with no additional consideration documented regarding:

- fraud risk assessment;

- insufficient documentation of discussions between the auditor and management;

- lack of evidence of the auditor’s assessment of fraud and

- lack of evidence of the auditor’s conclusions regarding fraud risk.

Accounting systems and controls (ISA 315)

The Coronavirus (COVID-19) has challenged client’s accounting systems and controls like nothing has ever before.

Audit firms need to consider whether the audit clients’ accounting systems and controls remain appropriate during Covid-19, especially with few or no client staff working from their office location. A common failing at monitoring visits is the carrying forward of systems notes from prior years with little evidence of written assessment of the impact of the Coronavirus on the accounting systems and controls. The notes on file must take account of the impact on the client’s operations of remote working and/trading in an online environment.

See Part 2 of this blog next week.

by John McCarthy Consulting Ltd. | Jul 30, 2021 | Blog, News

The various professional bodies are ramping up their anti-money laundering (AML) inspection regime, as there is more and more pressure coming at EU level, on professional bodies, to improve the consistency of the inspection system.

The main issues that are arising for Irish firms on recent AML inspections are:

- Lack of written procedures which evidence that firms are complying with AML regulations and legislation. These procedures ideally consist of an up to date AML Policies & Procedures Manual. Many firms have such policies and procedures already in place, but they are often out of date and do not clearly identify the MLRO. The latest changes to legislation came into effect on 23 April 2021 and the up to date AML Policies & Procedures Manual in use in the firm should reflect this.

- Client due diligence (CDD) – this consists of the following parts:

- Client verification – the ID obtained has not been signed and dated by the firm to evidence that they are ‘Certified Copies of the Originals’.

- Details of the client’s business, legal structure, sources of funds and geographic risks are often not properly recorded.

- Risk assessment and CDD procedures are not carried out prior to acting for the client.

- Firm-Wide Risk Assessment (often referred to as the Business-Wide Risk Assessment) – there is often little evidence that this written assessment (introduced in law since November 2018) has been completed or where it has been completed, the assessment is often not sufficiently detailed or up to date in accordance with Section 30A of the ‘Criminal Justice (Money Laundering and Terrorist Financing) Acts, 2010 to 2021’

- AML Compliance Review – Annual compliance review not completed or a inadequate review has been carried out. The review findings and implementation plan are extremely important. We carry out such external documented reviews for firms with advice on corrective action.

- Training – Appropriate AML training has not been undertaken by all relevant staff. We provide in-house and online AML Training delivered in a format tailored to each firm’s requirements.

- Annual Return declarations – Incorrect AML information disclosed on the firm’s Annual Return to its professional body. Attention to detail is important here and this will be reviewed as part of the AML Compliance Review we carry out.

by John McCarthy Consulting Ltd. | Jul 6, 2021 | Blog, News

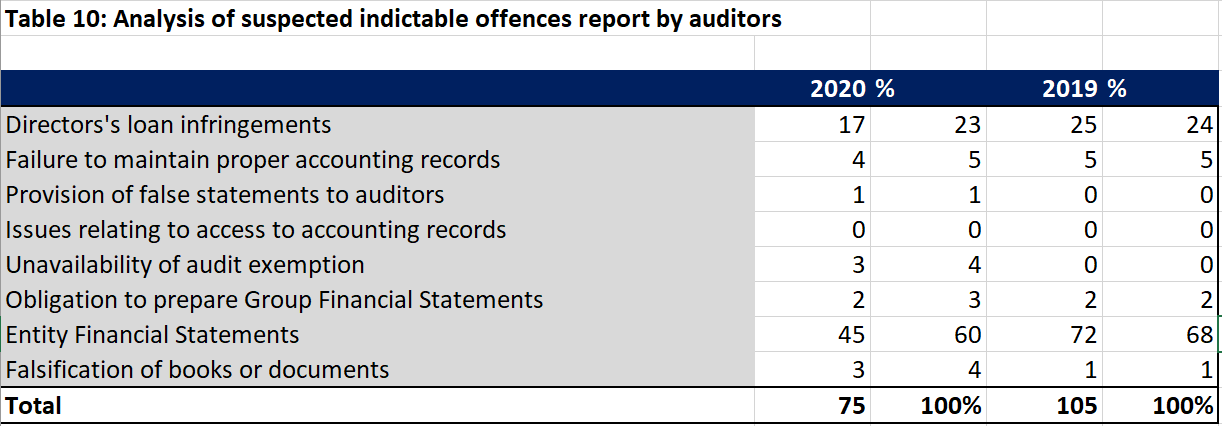

The Office of the Director of Corporate Enforcement (ODCE) recently published their Annual Report for 2020.

The section on the reporting by auditors of indictable offences, makes interesting reading, especially the fact that the greatest increase in reports for any category, has been to do with the falsification of books or documents. This particular category of offence is up from one incidence in 2019 to three in 2020. Perhaps connected with Covid?

The below table has the details. It should be noted that the number of reports received by the ODCE does not accord with the number of suspected offences reported as, in several instances, the report received includes reference to more than one suspected offence

These types of offence rarely occur in isolation and are often connected with money laundering, because the lack of/falsification of accounting records can often be used to conceal the money laundering activity. Where money laundering is suspected there is a requirement for simultaneous reporting to An Garda Síochana and Revenue, a topic we discussed in an earlier blog.

You can download and read the full ODCE report here.

For more about accountants’ AML compliance obligations, see our AML Policies, Controls & Procedures Manual for 2021.

The Manual contains all the latest requirements relevant to accountants contained in the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021 now fully in force.

For more blogs please visit this link and for our publications and manuals and services click on the hyperlinked words.

by John McCarthy Consulting Ltd. | Jul 5, 2021 | Blog, News

A recent article by the Independent revealed that a Rathfarnham family home address had been used in the registration of over 100 companies. See the full article here.

The article reports that two tenants resident at the address, had use the owner’s address without his knowledge. This highlights a major weakness in the CRO’s procedures for company set up where the trust placed in the ‘self-declaration’ process has been found wanting.

The Office of the Director of Corporate Enforcement (ODCE) and An Garda Siochana were contacted by the homeowner.

A spokesperson for the Department of Enterprise Trade and Employment which oversees the CRO confirmed that the CRO does not verify the identities of directors or secretaries of companies.

This latest development calls into question the serious lack of background verification carried out by the CRO which ensures that the Office never calls into question instances where multiple addresses are listed for the same director, not to mention the increased risk that these businesses could be used for money laundering activity.

A similar problem exists at UK Companies House where a consultation has been carried out called the ‘Corporate transparency and register reform’. Proposals include making companies using the FRS 105/102 accounts frameworks in the UK, declare their turnover, among other recommendations, to help verify that they genuinely qualify for these much reduced disclosure regimes. The results of the consultation have not yet been announced, but similar moves be follow in Ireland.

For more about accountants’ AML compliance obligations, see our AML Policies, Controls & Procedures Manual for 2021.

The Manual contains all the latest requirements relevant to accountants contained in the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021 now fully in force. Future blogs will look at various parts of the new and existing provisions of this legislation.

For more blogs please visit this link and for our publications and manuals and services click here.

by John McCarthy Consulting Ltd. | Jun 28, 2021 | Blog, News

The European Union has for some time, been trying to work out how best to combat financial crime that impacts EU finances.

Formally launched on 1 June this year, a new office, the European Public Prosecutor’s Office (EPPO) has been created. It was first established in 2017 with powers to investigate and prosecute crimes against the EU’s financial interests including money laundering.

The mandate of the EPPO’s is ‘to investigate, prosecute and bring to court crimes against EU budgets, such as fraud, corruption or serious cross-border VAT fraud’.

The EPPO’s Chief Prosecutor is Laura Codruța Kövesi, the former Chief Prosecutor of Romania’s National Anticorruption Directorate and former Romanian Prosecutor General.

Here is an interview with the new Chief Prosecutor.

The remaining EPPO staff consists of two Chief Deputies and other prosecutors drawn from the 22 participating EU countries. Unfortunately, Ireland is not participating in the EPPO along with Denmark, Hungary, Poland and Sweden. Sweden is said to join in 2022. Ireland have, however, signed up to the PIF Directive (2017/1371) which protects against the misuse of EU funds, and protecting EU taxpayer’s money. Ireland have the option to join the EPPO at any time.

The EPPO already faces a mountain of work, with over 3,000 reports submitted for action. According to Kövesi, the first new reports of alleged fraud against the EU budget, were submitted from Italy and Germany and arrived within hours of the EPPO’s online reporting system going ‘live.’ We wish Laura and her team success in the fight against financial crime.

For more about accountants’ AML compliance obligations, see our AML Policies, Controls & Procedures Manual for 2021.

The Manual contains all the latest requirements relevant to accountants contained in the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021 now fully in force. Future blogs will look at various parts of the new and existing provisions of this legislation.

For more blogs please visit this link and for our publications and manuals and services click here.